You’ve probably done the same late-night search many Inner West patients do. You look up Invisalign, love how discreet it is, start picturing straighter teeth in work meetings or family photos, and then hit the part that stops you cold. The price.

That moment can make treatment feel like something for “later”. After the renovation. After school fees settle down. After a few more pay cycles. For a lot of adults and parents, the issue is not whether Invisalign sounds worthwhile. It is whether the cost can fit into real life.

The good news is that an invisalign payment plan can turn one large cost into smaller, more manageable steps. In Australia, that often means combining a clinic payment plan with private health fund extras, so the total feels less intimidating and more practical.

For people in Dulwich Hill, Marrickville, Ashfield, Petersham, Summer Hill, Lewisham and the wider Inner West, the biggest confusion is usually not the treatment itself. It is the financial pathway. How much is due first? Can health insurance help? Is an outside lender necessary? What happens if a plan sounds interest-free but is not?

This guide is written to make those answers clear, in plain English, with the same calm, step-by-step approach we use in the chair. If you’d like to learn more about your local dental options, you can also visit The Smile Spot.

Your Dream Smile Is More Accessible Than You Think

A common story goes like this. Someone has been thinking about straightening their teeth for years. They finally decide to look into clear aligners because metal braces feel too visible for work, social events, or day-to-day confidence. Then they see the total treatment cost and assume they need all of that money ready upfront.

Most of the time, that assumption is the primary barrier.

In practice, payment plans change the conversation. Instead of asking, “Can I afford the full amount today?”, patients start asking a better question. “What would this look like month to month after my health fund rebate?”

That shift matters. It turns Invisalign from a big, abstract expense into something you can compare with the rest of your household budget.

Why cost feels more confusing than treatment

Many understand the treatment basics fairly quickly. Clear aligners move teeth gradually. You wear them in sequence. You come in for reviews. Simple enough.

The finances feel murkier because several moving parts can apply at once:

- Clinic fees: Your quote may include scans, treatment planning, aligners, and review visits.

- Health fund extras: Orthodontic benefits can reduce the amount you pay yourself.

- Payment structure: A deposit and regular instalments often replace one large upfront bill.

- Different lenders: Some clinics use in-house plans, while others offer outside finance options.

A smile plan is easier to commit to when the numbers are explained as clearly as the treatment.

For many Inner West households, affordability is not just about the sticker price. It is about timing, flexibility, and knowing exactly what is included before you begin.

What Exactly Is an Invisalign Payment Plan

An invisalign payment plan is a way to split treatment costs into smaller payments over time rather than paying the full amount at once.

It can be seen as a structured subscription for your smile. You begin with a deposit, then pay the balance in regular instalments while treatment is underway. The treatment is clinical. The payment plan is administrative. But the two are connected because spreading out the cost often makes it easier to start without delay.

How the basic structure usually works

In Australia, clinics commonly use an in-house arrangement with an initial deposit, then ongoing instalments. According to Fiesta Orthodontics, Australian dental clinics often structure in-house financing with a typical $500 to $1,000 initial deposit followed by instalments over 12 to 24 months at 0% interest for eligible patients, and this approach is associated with 25% to 40% higher case acceptance rates.

That tells you two useful things as a patient. First, a deposit is normal. Second, regular instalments are normal too.

A simple plan often looks like this:

- Consultation and quote: Your teeth are assessed and a treatment plan is prepared.

- Initial deposit: This helps get the case started.

- Regular payments: These may be fortnightly or monthly.

- Completion of balance: The account is finalised over the agreed term.

If you want a broader look at orthodontic options, this article on orthodontics and smile planning is a helpful next read.

Why clinics offer payment plans

The reason is straightforward. Orthodontic treatment is valuable, but a single lump-sum payment can feel too heavy even for households that are financially stable.

An instalment structure does three things:

- Reduces upfront pressure

- Makes budgeting simpler

- Lets patients start sooner rather than postponing treatment

What patients often misunderstand

People sometimes assume “payment plan” means “loan”. Not always.

Some plans are arranged directly with the clinic. Others involve a third-party finance provider. Those are different products with different risks, approval steps, and fee structures. The phrase sounds similar, but the experience can be very different.

Before agreeing to any invisalign payment plan, ask one clear question. “Is this in-house, or is this third-party finance?”

That one question usually clears up most confusion in under a minute.

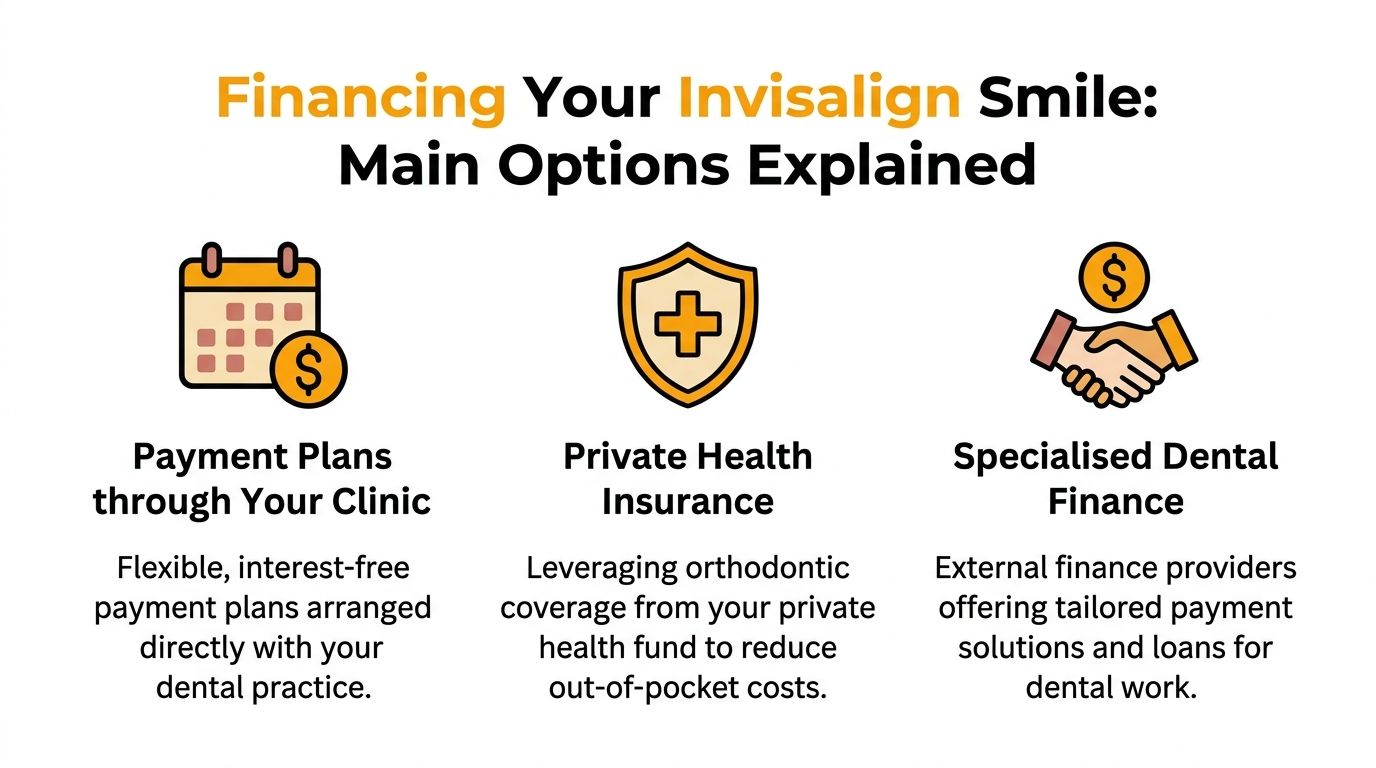

Financing Your Smile Your Main Options Explained

When Inner West patients ask about paying for Invisalign, there are usually three pathways worth comparing. Each can work. The best one depends on your budget, your health fund, and how much flexibility you want.

Payment plans through your clinic

This is often the easiest model to understand. You deal directly with the dental practice, pay a deposit, and then continue with scheduled instalments.

The attraction is simplicity. Patients usually prefer a plan that feels transparent and easy to follow, especially when they are already making a health decision.

Typical advantages include:

- Clear structure: You know the amount, frequency, and term from the start.

- Potentially interest-free terms: Many clinics offer 0% plans for eligible patients.

- Less friction: There is usually less paperwork than with an external lender.

The key question to ask is whether every cost is already included in the quote, or whether some items sit outside the plan.

Private health insurance extras

This is the area that causes the most confusion, especially because so much online advice is written for the US rather than Australia.

According to Cherry’s overview of Invisalign payment planning in Australia, Australian private health insurance extras often cover 50% to 100% of orthodontic treatments like Invisalign up to annual or lifetime limits, but these policies typically require Major Dental cover and waiting periods.

That means your policy may help significantly, but it will not usually be as simple as “insurance covers it” or “insurance does not cover it”. The fine print matters.

Common issues to check:

- Waiting period: Have you served it yet?

- Orthodontic limits: Is there a lifetime cap?

- Policy type: Does your extras cover include orthodontics?

A health fund rebate reduces the amount you need to finance. It does not automatically replace a payment plan.

If you are also researching broader finance models online, some readers like comparing local dental arrangements with an alternative inteligente de finanțare to understand how different payment structures work in plain terms.

For a local guide focused on affordability, this post on dentists with payment plans near me can help frame the options.

Specialised dental finance

This route uses an outside lender rather than the clinic itself. It can be helpful when a patient wants a separate finance product or a different repayment term.

It can also be more complex.

External finance may involve:

- a formal application

- credit assessment

- fees or interest depending on the lender

- repayment terms that feel less flexible than an in-house arrangement

That does not make it wrong. It just means you should treat it as finance first, dental second. Read the terms carefully.

Which option tends to suit which patient

Consider this simplified guide:

| Option | Best fit for |

|---|---|

| In-house clinic plan | Patients who want clarity and straightforward instalments |

| Health fund plus clinic plan | Patients with strong extras cover who want to reduce out-of-pocket cost |

| Third-party dental finance | Patients who prefer or need an external lending arrangement |

For many Australian patients, the most practical combination is a health fund rebate first, then a clinic plan for the remaining balance.

Invisalign Cost Examples and Payment Breakdowns in Sydney

Numbers make this much easier to grasp.

According to Dental Park Care’s Invisalign cost guide, Invisalign treatment in Australia can start from AUD $4,095 for standard cases, with higher costs for more complex treatment. The same source notes average insurance coverage of around $1,772 for eligible patients, and says monthly payments can be as low as $58 over 24 months.

That gives us a useful framework for a Sydney-style example.

A sample breakdown using the verified figures

Below is a simple illustration based on the verified standard-case figure and average insurance figure above.

Sample Invisalign Payment Plan Breakdown (18-Month Treatment)

| Cost Component | Amount (AUD) |

|---|---|

| Standard Invisalign treatment | $4,095 |

| Average insurance coverage for eligible patients | $1,772 |

| Remaining out-of-pocket amount | $2,323 |

That remaining balance is the number many patients need to plan around, not the original quote.

How to read a quote without getting lost

A dental quote can feel dense if you are seeing one for the first time. Focus on these items first:

- Total treatment fee: The starting figure before rebates.

- Expected health fund contribution: What may be claimable, if your policy allows.

- Net patient amount: What remains after insurance.

- Repayment timing: Whether instalments are fortnightly or monthly.

A lot of patients find it easier when they compare dental planning to routine care. If you already budget for check-ups and preventive visits, this article on a check-up and clean is a good reminder that oral health costs are often easiest to manage when they are planned rather than reactive.

Why examples matter more than averages

Two people can both ask for “Invisalign cost” and receive very different answers. One may need a relatively straightforward alignment. Another may need a more involved plan.

That is why sample figures are useful, but personal quotes matter more.

The most useful number is not the advertised cost. It is your own likely out-of-pocket amount after checking your fund.

If your policy contributes well, the practical monthly commitment can feel far more manageable than expected. If your policy does not, a payment plan may still make treatment realistic by spreading the cost into smaller instalments.

Navigating Eligibility and Application Steps

Once patients understand the cost pathways, the next concern is usually approval. Not everyone wants to apply for finance, and not every type of finance works the same way.

A calm, step-by-step process makes this part much easier.

Step one, get a proper clinical assessment

Start with the dental side, not the finance side.

The sequence should be:

- Consultation first: Check whether Invisalign is appropriate for your teeth and bite.

- Digital records: Scans and photos help shape the treatment plan.

- Written quote: You need a clear fee before discussing payment options.

Without that quote, any financial discussion is just guesswork.

Step two, check your health fund properly

If you have extras cover, ask the clinic team to help you confirm what applies to orthodontics. Patients often assume “extras” means automatic coverage, but that is not always how policies work.

Useful questions include:

- Does my policy include orthodontics?

- Have I served the waiting period?

- Is there an annual or lifetime limit?

- Can claims be processed on the day?

Step three, compare in-house and third-party approval pathways

This is the part where many people need plain English, not finance jargon.

According to NK Orthodontics, about 15% of Australians face rejection from third-party dental lenders due to credit scores under 600, and 1 in 5 users incur high fees if they default, which is why interest-free in-house clinic plans may be a safer option for many patients.

That does not mean external finance is always unsuitable. It means you should understand the trade-off before applying.

A simple comparison:

| Pathway | What to expect |

|---|---|

| In-house clinic plan | Often more direct and easier to understand |

| Third-party lender | May involve credit checks, separate terms, and default fees |

If a lender says yes quickly, still read the repayment terms slowly.

A short video can also help if you prefer to see the treatment side explained visually before making financial decisions.

Step four, ask these questions before signing

Bring these to your consultation:

- Is the quote all-inclusive?

- How often are repayments due?

- What happens if I miss a payment?

- If treatment changes, how is that handled?

- Is this payment plan run by the clinic or a finance company?

Patients rarely regret asking more questions. They often regret assuming they understood the paperwork when they did not.

How The Smile Spot Makes Your Invisalign Journey Seamless

The best financial experience in dentistry is usually the one that feels simple from the patient’s side.

At a practical level, that means you should be able to understand your quote, know what your health fund may contribute, and have your remaining balance explained in a way that feels ordinary rather than stressful. A clinic team should make this easier, not more confusing.

Fewer moving parts for the patient

One reason local patients value a well-organised clinic process is that it removes hand-offs. You do not want to chase one person for a quote, another for a rebate estimate, and someone else for payment timing.

According to Invisalign’s insurance and payment information, clinics that integrate with major health funds like Bupa and NIB can process claims for orthodontic limits of AUD $600 to $2,000 at the point of service, leading to a 20% to 35% cost reduction for patients.

That kind of integration matters because it shortens the path between “I’m interested” and “I understand exactly what I need to pay.”

What patients tend to value most

For busy people in the Inner West, the smoothest experience usually includes:

- Transparent quotes: Clear inclusions, clear exclusions, no vague language.

- Health fund help: Staff who understand how to check and apply benefits.

- Flexible scheduling: Easier to manage around work, school, and commuting.

- Supportive care: A steady approach that keeps both treatment and payments understandable.

Patients exploring other cosmetic options often appreciate the same clarity when reading about professional teeth whitening, because confidence treatments should feel well explained from start to finish.

Why this matters beyond the money

People often think the payment conversation is separate from the treatment journey. In real life, they affect each other.

When finances are clear, patients feel more comfortable starting. When they feel comfortable starting, they are more likely to stay engaged, attend appointments, and move through treatment with less stress.

That is what a seamless experience really means. Not flashy finance. Just fewer surprises.

Frequently Asked Questions About Invisalign Payments

Are retainers included in an invisalign payment plan

Often, they are included in the overall treatment plan, but you should never assume. Ask for a written quote that shows exactly what is covered.

Look for mention of:

- Post-treatment retainers

- Review appointments

- Refinement aligners if needed

- Any replacement costs

The more detailed the quote, the fewer surprises later.

Can I combine private health insurance with a payment plan

Yes, that is commonly how patients make treatment more manageable. The health fund rebate can reduce the amount you need to pay yourself, and the remaining balance may then be spread over instalments.

The important part is confirming your orthodontic entitlement before the plan is finalised.

What if I move during treatment

This is not unusual. If you relocate, your current provider can generally coordinate records and treatment details for a transfer. The financial side depends on the terms of your agreement and how much treatment has already been completed.

Ask early if a move is even a possibility.

Can I use superannuation for Invisalign

In some situations, patients explore early release of superannuation on compassionate grounds for dental treatment. Whether that applies depends on the clinical circumstances and the relevant application process.

If you are considering it, get advice on eligibility and documentation before relying on that pathway.

What if treatment takes longer than expected

This depends on the terms of your treatment plan, not just the calendar. Some quotes are designed around the full course of treatment rather than a strict time window.

Ask these two questions:

- Are refinements included?

- Does the payment plan change if treatment runs longer?

The safest payment plan is the one you understand before the first aligner is made.

Is third-party finance always a bad idea

No. It can suit some patients. But it should be reviewed carefully because the approval process, fee structure, and consequences of missed payments may be different from an in-house arrangement.

If you are choosing between the two, simplicity is often an underrated advantage.

If you’re considering Invisalign and want clear, local guidance on costs, rebates, and payment options, The Smile Spot can help you understand the process without the jargon. A well-explained plan can make a straighter smile feel far more achievable than you might expect.

")