You've probably had the same thought more than once. You catch your smile in a photo, notice chipped edges, uneven shape, staining that whitening won't shift, and start wondering whether veneers could finally give you the look you want. Then the practical question arrives just as quickly: how do you pay for it without putting pressure on the rest of your life?

That's where a veneer payment plan matters. For many people, the issue isn't whether veneers are worth considering. It's whether the upfront cost fits into a real household budget right now. A clear plan can turn the decision from overwhelming into manageable.

Making Your Dream Smile a Reality

A smile makeover often feels like something to put off. Not because the result doesn't matter, but because the bill arrives all at once while the benefit is meant to last far longer. That mismatch is why payment plans make sense in cosmetic dentistry.

People already spread out other meaningful expenses. They finance cars, home updates, elective medical treatments, and major appliances because the full amount in one payment doesn't always reflect how people manage money month to month. Veneers fit that same pattern.

Why payment plans matter in Australia

In Australia, Medicare doesn't cover veneers because they're typically a cosmetic procedure, so patients generally need to self-fund or use finance. The same source notes that average full-time weekly earnings were A$2,010.80 in May 2024, which helps explain why a full veneer case can exceed what many households can comfortably pay at once (Australian veneer payment plan context).

That doesn't mean veneers are out of reach. It means the financial structure matters just as much as the clinical plan.

Practical rule: If the treatment suits your smile goals but the upfront bill would disrupt rent, mortgage, school costs, or savings, a structured payment plan is usually the more sensible path than trying to force a one-off payment.

What a good plan changes

A well-designed veneer payment plan does three useful things:

- It creates predictability. You know what you're committing to and when payments are due.

- It lowers decision pressure. You can focus on whether veneers are clinically right for you, not only whether you can pay everything today.

- It protects your wider budget. Spreading the cost can be easier than draining savings meant for emergencies or family expenses.

The main point is simple. Improving your smile shouldn't require financial chaos. With the right repayment structure, cosmetic treatment becomes something you can approach calmly and realistically.

What Exactly Is a Veneer Payment Plan

A veneer payment plan is an arrangement that splits the cost of treatment into smaller repayments over an agreed period. Instead of paying the full amount on the day treatment starts, you pay in instalments that are easier to absorb.

The easiest comparison is a home improvement project. Renovating a kitchen isn't typically considered a single cash event if financing is available. Instead, the focus is on total cost, timeline, and what the ongoing payment will look like. Veneers work much the same way.

How it works in practice

The process is usually straightforward:

- Your dentist assesses the treatment. This includes the number of teeth involved, the type of veneer, and whether any preparation is needed first.

- A total fee is set out clearly. You should know what's included before agreeing to anything.

- Repayments are structured. These may be weekly, fortnightly, or monthly depending on the plan.

- Treatment starts under the agreed terms. Some plans are arranged directly with the clinic, while others are handled by an external finance provider.

If you're still deciding whether veneers are even the right cosmetic option, it helps to first understand dental veneers in Dulwich Hill and what the treatment involves.

How this differs from using a credit card

A payment plan isn't automatically the same as putting dentistry on a credit card. That distinction matters.

A dedicated dental finance arrangement is usually more structured. It tends to involve a clear repayment schedule and a defined purpose. A credit card, by contrast, can blur into everyday spending, which makes it easier to lose track of the true cost of treatment over time.

The best finance option is the one you can explain to yourself in one sentence: what you're paying, how often, for how long, and what happens if you miss a payment.

That clarity is what patients should look for. If the terms feel vague, rushed, or difficult to understand, it's worth slowing down before committing.

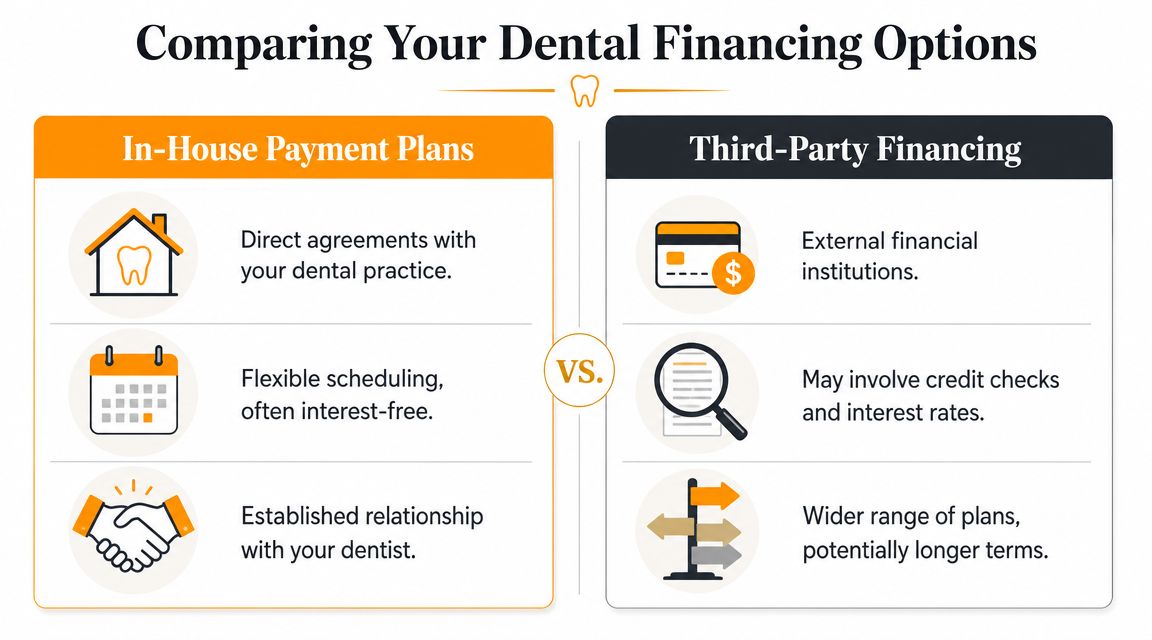

Comparing Your Dental Financing Options

There isn't one universal way to pay for veneers. The right option depends on how your treatment is structured, how quickly you want to complete it, and how comfortable you are with the repayment terms.

The three main paths

Most patients compare three broad options:

In-house payment plans

These are arrangements made directly with the clinic. They can be simpler to discuss because the dental team already understands your treatment plan and scheduling.Third-party finance or BNPL

These plans are run by external lenders or payment providers. They can offer a wider range of terms, but approval criteria, fees, and conditions may differ.Private health fund support

Health funds generally don't replace the need for payment planning in cosmetic cases, but they may still affect overall out-of-pocket costs in some situations. The practical value depends on your cover and the nature of the treatment.

For a broader view of how businesses think about instalments and affordability, Tagada's insights on payment strategies are a useful read. The same principle applies in dental care: payment design changes whether a service feels accessible or stressful.

Veneer payment options at a glance

| Financing Option | Best For | Key Considerations |

|---|---|---|

| In-house payment plans | Patients who want direct communication with the clinic | Terms may be simpler to discuss, but availability varies by practice |

| Third-party financing | Patients who want more plan variety or longer repayment options | May involve approval checks, fees, interest, or stricter conditions |

| BNPL-style services | Smaller treatment stages or short repayment windows | Can look manageable at first, but missed payments or tight budgets can create pressure |

| Private health fund contribution | Patients with relevant extras cover or mixed treatment needs | Usually doesn't remove the need for private payment for cosmetic veneers |

A related consideration is whether the repayment approach suits other cosmetic treatments too, which is why some patients also compare plans used for Invisalign payment options.

Match the plan to the veneer type

This is one of the most overlooked parts of financing. The repayment term should fit the treatment, not just the monthly number.

The guidance most worth paying attention to is this: porcelain veneers involve a higher upfront investment but generally last longer, while composite veneers are usually less expensive but have a shorter lifespan. That's why a longer term may suit porcelain, while a shorter interest-free period can make more sense for composite. The same Australian guidance also notes that ongoing maintenance sits outside the original finance contract and should be factored into affordability (finance considerations for porcelain and composite veneers).

Here's a short explainer if you'd like to hear another perspective before comparing plans:

A plan works best when it matches both your smile goals and your real budget. A low monthly figure isn't automatically a good deal if the structure doesn't fit the treatment you're receiving.

Understanding Veneer Costs and Eligibility

The question patients ask most often is simple: what will veneers cost me? The honest answer is that there isn't one standard figure that suits every case. Veneer treatment is customised, and the financial side follows the clinical side.

What changes the total cost

Several factors influence the final treatment fee:

Number of teeth

A single veneer and a broader smile design are very different financially. Cosmetic cases often involve multiple teeth, which changes the scope quickly.Material choice

Porcelain and composite don't behave the same clinically or financially. Each has a different balance of appearance, longevity, maintenance, and cost.Preparation and supporting treatment

Some patients need preliminary dental work before veneers are appropriate. That can affect timing and total spend.Design complexity

Small shape corrections are different from a full visible-smile transformation where symmetry, bite, and colour matching all matter.

The Australian Dental Association guidance commonly cited by clinics is that veneer treatment is typically paid for privately, and the financing need often grows because cosmetic work commonly covers multiple teeth rather than one isolated tooth (private payment context for veneer treatment).

For a more detailed local discussion of treatment variables, this guide to porcelain veneers cost in Australia is a useful starting point.

What approval usually depends on

Eligibility for a payment plan depends on the provider, but patients are commonly asked for practical proof that repayments are manageable. That may include identity checks, income evidence, and a review of existing financial commitments.

Approval isn't the only question worth asking. Suitability matters just as much.

A payment plan should support treatment, not create strain that follows you long after the excitement of a new smile wears off.

A sensible affordability check

Before you apply, ask yourself:

- Can I meet the repayments comfortably? If the answer depends on everything going perfectly each month, the plan may be too tight.

- Am I already carrying other short-term debt? Elective treatment is different from urgent care. It should sit within a stable budget.

- Would a staged approach help? In some cases, spacing treatment or considering a simpler cosmetic option first is the wiser move.

Patients usually feel more confident once cost is framed as a personalised plan rather than a mystery number.

Your Path to Veneers at The Smile Spot

Patients don't need more general advice. They need a clear next step, a transparent quote, and someone who can explain the financial options without making the process feel heavy.

At The Smile Spot, the practical path starts with a proper assessment, not a rushed promise. Veneers are a cosmetic treatment, but the decision still has to be grounded in oral health, bite function, material choice, and what repayment style actually fits your circumstances.

What the local process looks like

For Inner West patients, the journey is usually easier when it's broken into clear stages:

Consultation first

Your smile goals, current dental condition, and suitability for veneers are reviewed carefully.A written treatment plan

This sets out what type of veneer is being considered, how many teeth are involved, and what costs sit around the treatment.A finance discussion that matches the plan

That may include in-house arrangements or third-party options where appropriate. The point is to find a structure that fits the case, not to force every patient into the same format.Clarity about health funds

Patients often need help understanding whether their private cover changes any part of the out-of-pocket cost.Booking with confidence

Once the treatment and payment path are clear, the process feels far less daunting.

If you're weighing veneers against other smile improvements first, this overview of cosmetic dental treatment can help you compare the broader options.

Where caution matters

Accessible finance can be useful, but it isn't automatically harmless. Australian-facing guidance on dental payment plans warns that BNPL can create debt stress, especially for financially vulnerable users, and that elective treatment should only be financed if the repayments are genuinely affordable. In some cases, delaying treatment or choosing a more conservative option is the smarter short-term decision (BNPL cautions for veneer patients).

The right answer isn't always “yes, finance it now”. Sometimes the right answer is “not yet”, “stage the treatment”, or “choose a different material”.

That's part of responsible treatment planning too.

A straightforward first appointment

A consultation works best when it gives you answers, not pressure. The complete care package at $240 includes an exam, X-rays, scale and fluoride, which gives patients a practical way to start with full information before deciding on cosmetic work.

That first visit is where a veneer payment plan becomes concrete. You're no longer guessing. You can see the treatment scope, understand the likely pathway, and decide whether now is the right time.

Take the First Step Towards Your New Smile

A new smile doesn't have to stay in the “maybe one day” category. If veneers are the right treatment for your teeth and your goals, a well-structured payment plan can make the process feel organised rather than stressful.

The important part is choosing carefully. Look at the treatment itself, the number of teeth involved, the material being used, the maintenance you'll need later, and whether the repayment schedule fits your normal life without strain. That's what turns a veneer payment plan from a tempting offer into a sensible decision.

If you're still comparing possibilities, this guide on dentists with payment plans near me can help you think through what good financial guidance should look like in a dental setting.

A consultation is the easiest place to begin. You can discuss your smile goals, find out whether veneers are suitable, and get a personalised plan that makes sense clinically and financially. That's usually all people need to move from uncertainty to a clear next step.

If you're ready to explore veneers with a personalised treatment and payment approach, book a consultation with The Smile Spot. The team can walk you through suitability, treatment options, likely costs, and the repayment pathways available so you can make a calm, informed decision.

")